Why Nebius Is Perfectly Positioned For The Open-Source AI Shift (Archive)

Nebius Group expands infrastructure and capitalizes on high-margin open-source AI enterprise compute demand.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. I also publish full 5-Minute Pitches on this site. This will be behind a paywall, accessible to Hunter Tier members.

Elevator Pitch

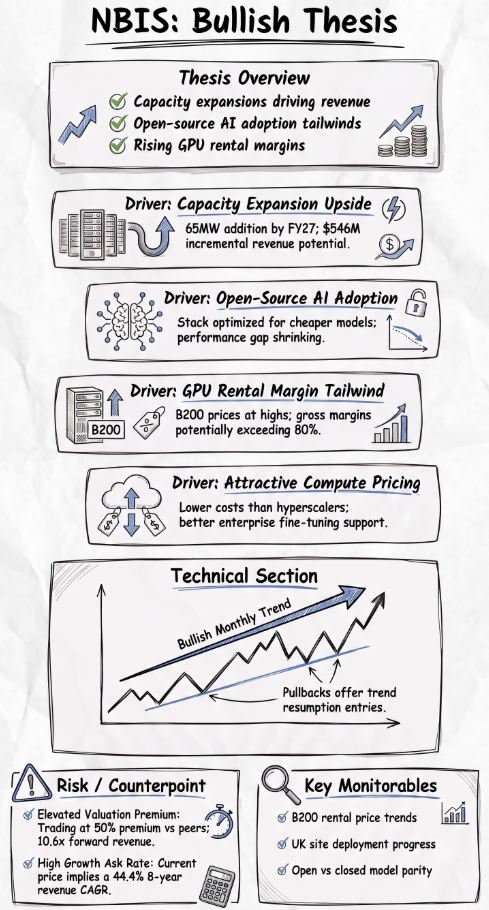

- Nebius plans a 65MW infrastructure expansion across three UK sites by FY27, which is projected to generate $546 million in incremental revenue.

- Enterprise demand for cheaper open-source AI models benefits Nebius due to its optimized cloud stack and highly competitive compute pricing compared to major legacy hyperscalers.

- Soaring Nvidia B200 GPU rental prices combined with short-duration contracts provide a significant tailwind that could expand the company's gross margins above 80%.

- NBIS stock trades at a premium 1-yr fwd EV/Revenue multiple of 10.6x, requiring an aggressive 44.4% 8-yr revenue CAGR to justify its current valuation.

- Technical analysis indicates a sustained long-term monthly uptrend, with recent price pullbacks offering healthy entry points before the broader upward trajectory resumes.

Read the full article here.