Micron: This Memory Cycle Is Only Getting Stronger (Archive, Full Access)

Micron benefits from structural tailwinds driven by tight DRAM and NAND market conditions.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. I also publish full 5-Minute Pitches on this site. This will be behind a paywall, accessible to Hunter Tier members.

Elevator Pitch

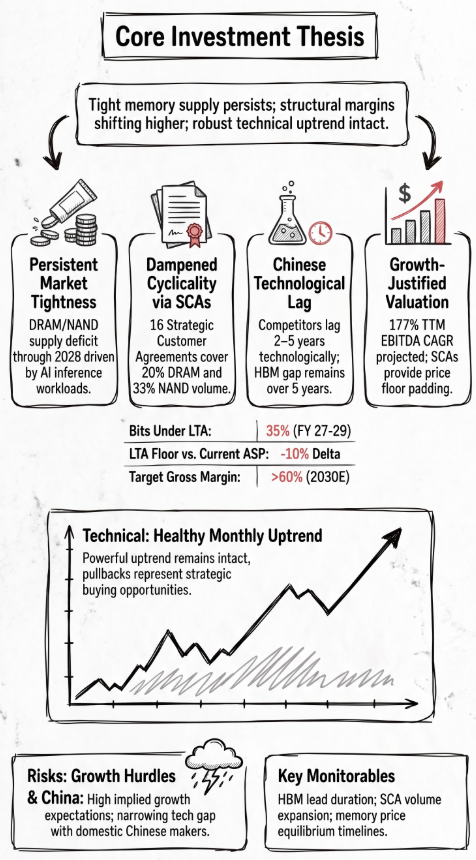

- Micron benefits from structural tailwinds as tight DRAM and NAND market conditions are expected to persist until at least post-2028 due to surging AI inference workloads.

- Long-term strategic customer agreements now cover 20% of DRAM and 33% of NAND volume, stabilizing pricing and driving projected gross margins above 60% by 2030.

- Emerging Chinese competitors are expanding market share but remain technologically lagged by 2 to 5 years and pose minimal threat as their supply is contained domestically.

- MU stock needs a 22.6% 10-year EBITDA CAGR to justify its current market price. With a 177% CAGR for the annual EBITDA growth rate through FY28, growth is on track to meet expectations.

- Technical analysis confirms a robust long-term monthly uptrend, establishing clear support levels where equity pullbacks present high-probability buying opportunities for investors.

Read the full article here.