Portfolio Performance - Apr'26

Apr'26: ~7.7% annualized alpha, Sortino 2.0, IR 0.73, low drawdowns. Live, real-money portfolio.

Portfolio context is detailed in the About page.

Performance metrics here are for the 1 Jul'24 to 30 Apr'26 time period.

Summary

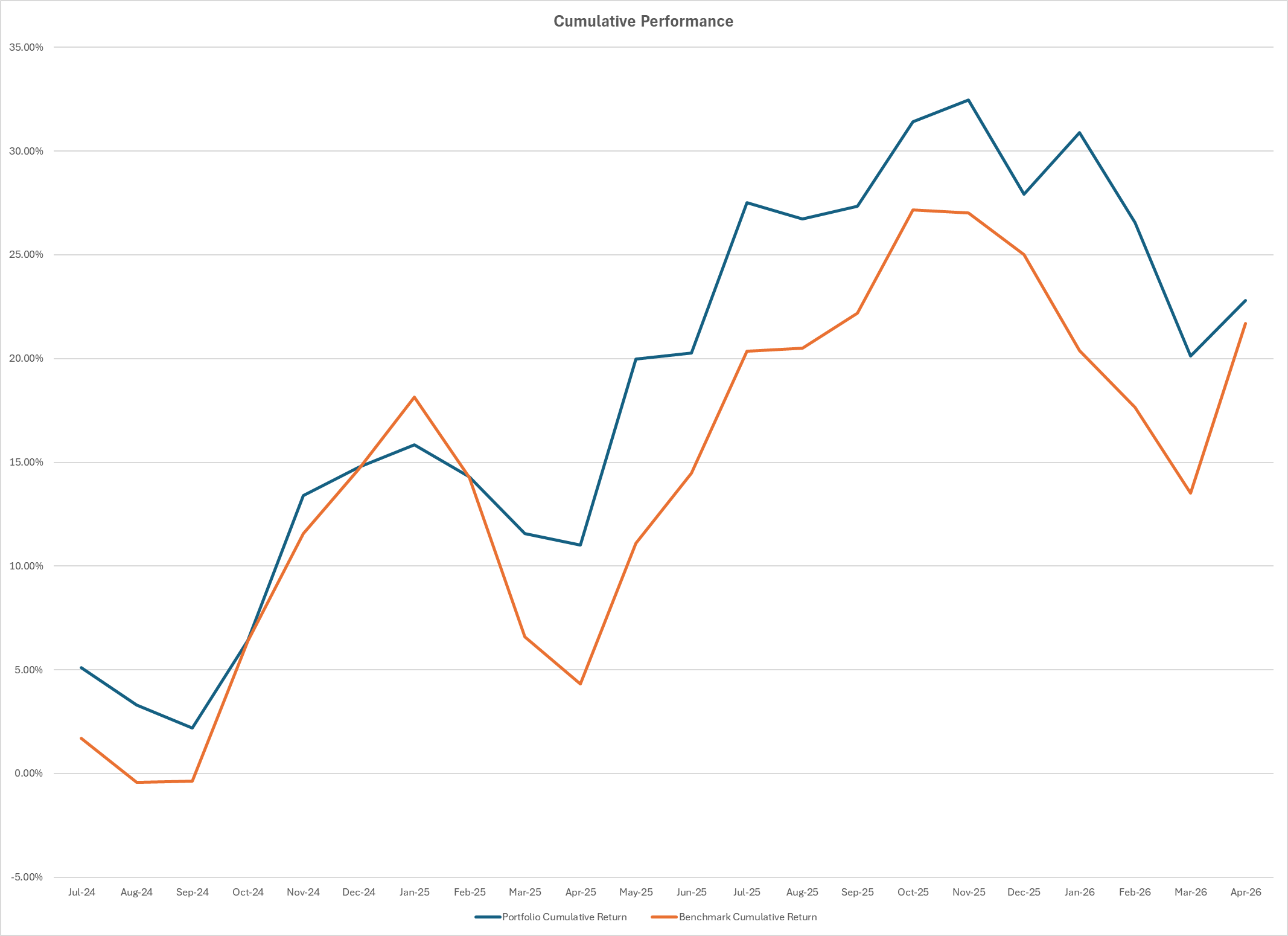

Monthly performance dashboard

Strong risk-adjusted performance metrics

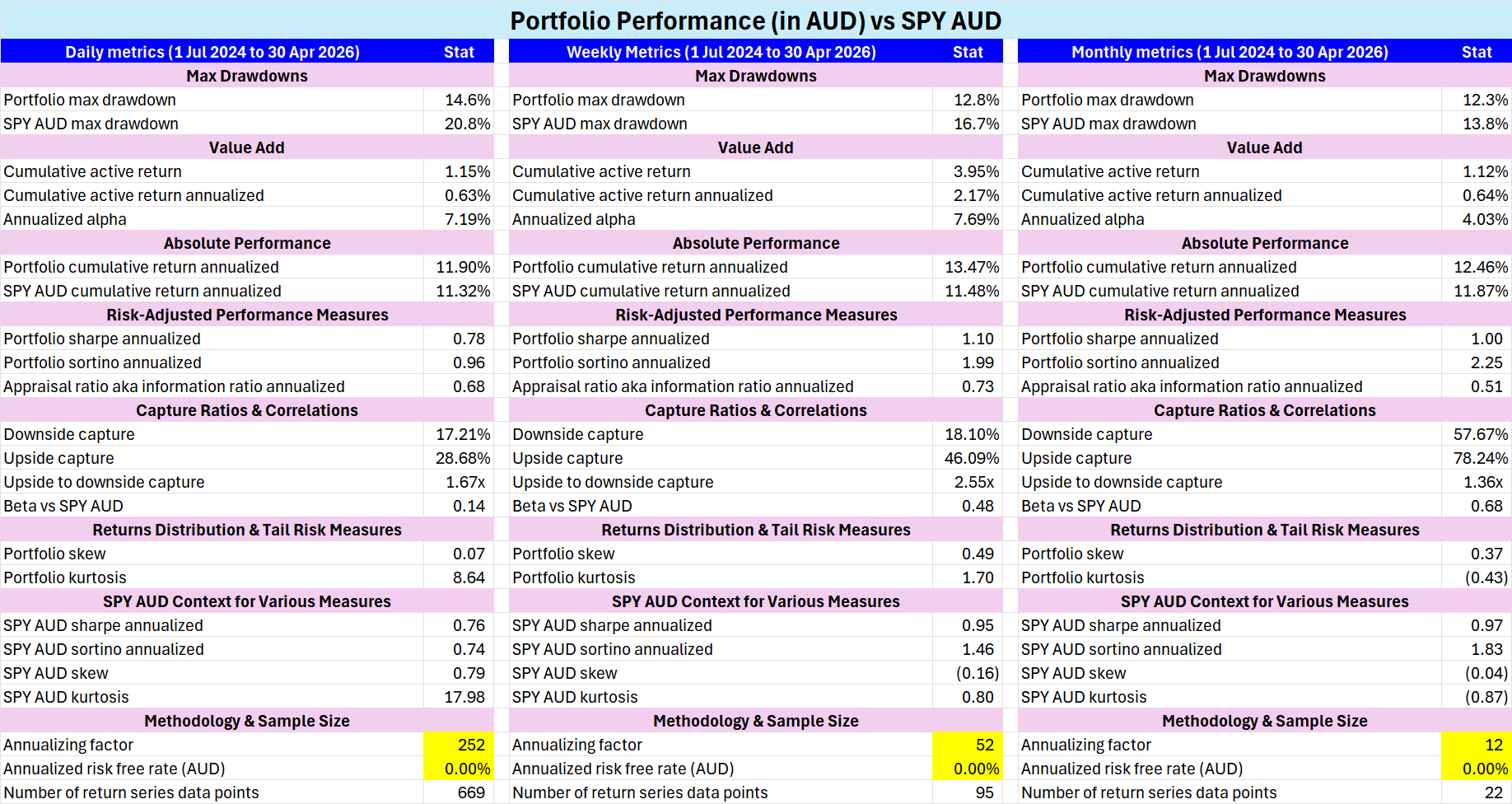

- Daily/weekly Sharpe: 0.78/1.10, assuming 0% risk-free or hurdle rate.

- Daily/weekly Sortino: 0.96/1.99, assuming 0% risk-free or hurdle rate.

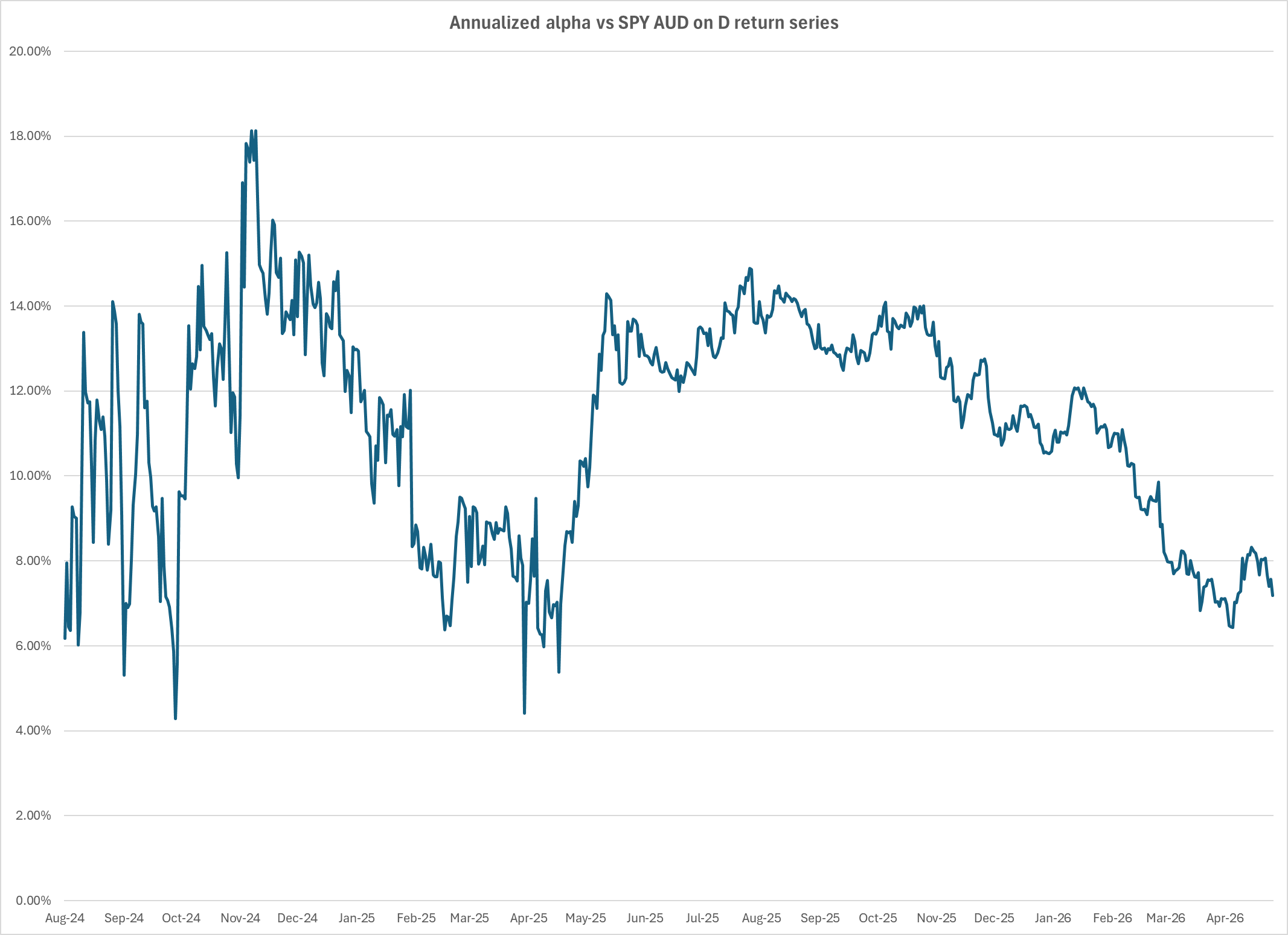

- Daily/weekly annualized alpha: of 7.2%/7.7% vs SPY AUD benchmark.

Value addition measures are high.

Results are based on a very large, diverse sample size

- Average of 133 tickers bet on over 22 months.

- Aggregate returns profile is made up of many contributions of small positions rather than a reliance on a few concentrated winners.

Diverse sources of returns reduces dependency on favorable market regimes.

Minimal catastrophic tail risk and scalable

- Long-only, zero leverage strategy investing in global stocks and related traditional ETFs without any inverse, ETN or other derivative exposures in mostly Developed markets.

- Positive skew in both overall portfolio and ticker-level return, contribution to return distributions.

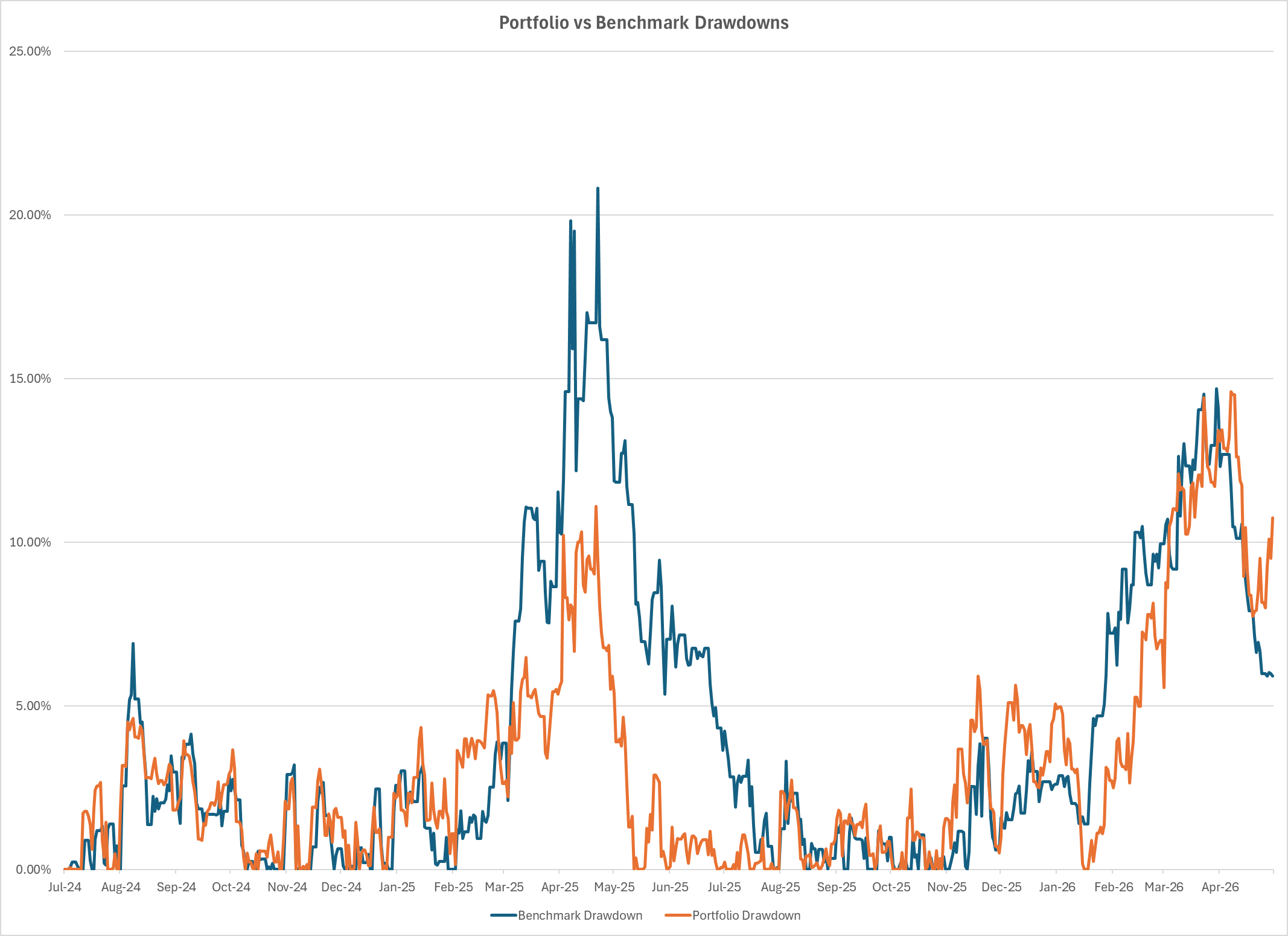

- Low max drawdowns, low beta, upside to downside capture ratio of 1.5-2.5x.

- Market impact analysis suggests this portfolio is largely scalable to >USD 100M AUM.

The strategy is suitable to manage a large amount of capital in order to grow wealth over a long period of time with dramatically reduced volatility along the way.

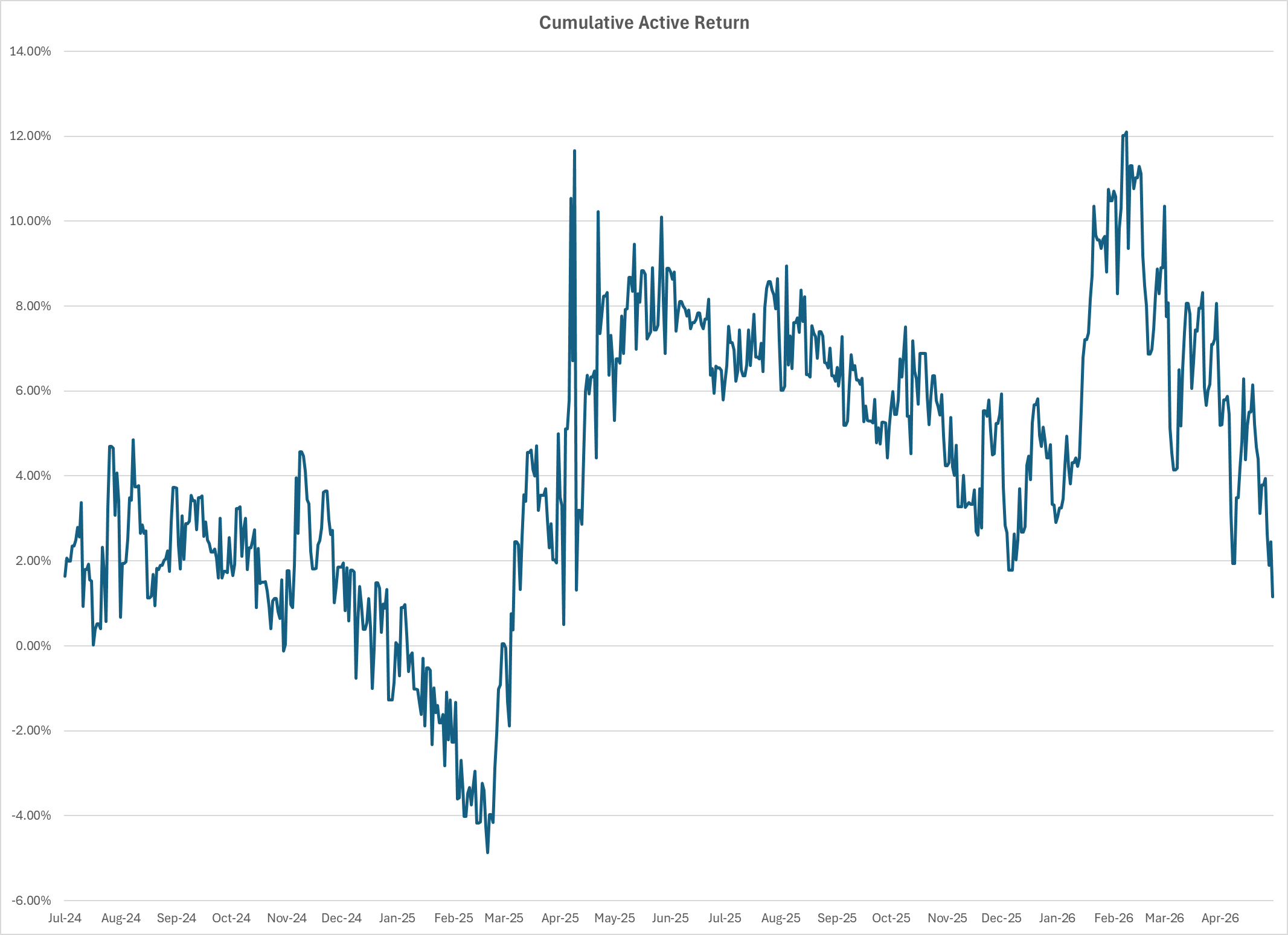

Performance vs SPY AUD

Portfolio (AUD) vs SPY AUD

These metrics are computed using an annualized AUD risk-free/hurdle rate of 0%, which is an industry standard for comparability purposes.

- Much lower max drawdowns vs SPY AUD benchmark

- >5% annualized alpha vs SPY AUD benchmark in daily and weekly timeframes

- High upside-to-downside capture, indicating a highly convex (asymmetric) return profile vs SPY AUD.

Active Stock Pick Selection Analytics

- Overall win rate averages are in the low 40%, but average win is almost 2x average loss, leading to a profit factor of 1.4-1.6.

More Details on Portfolio Performance Profile

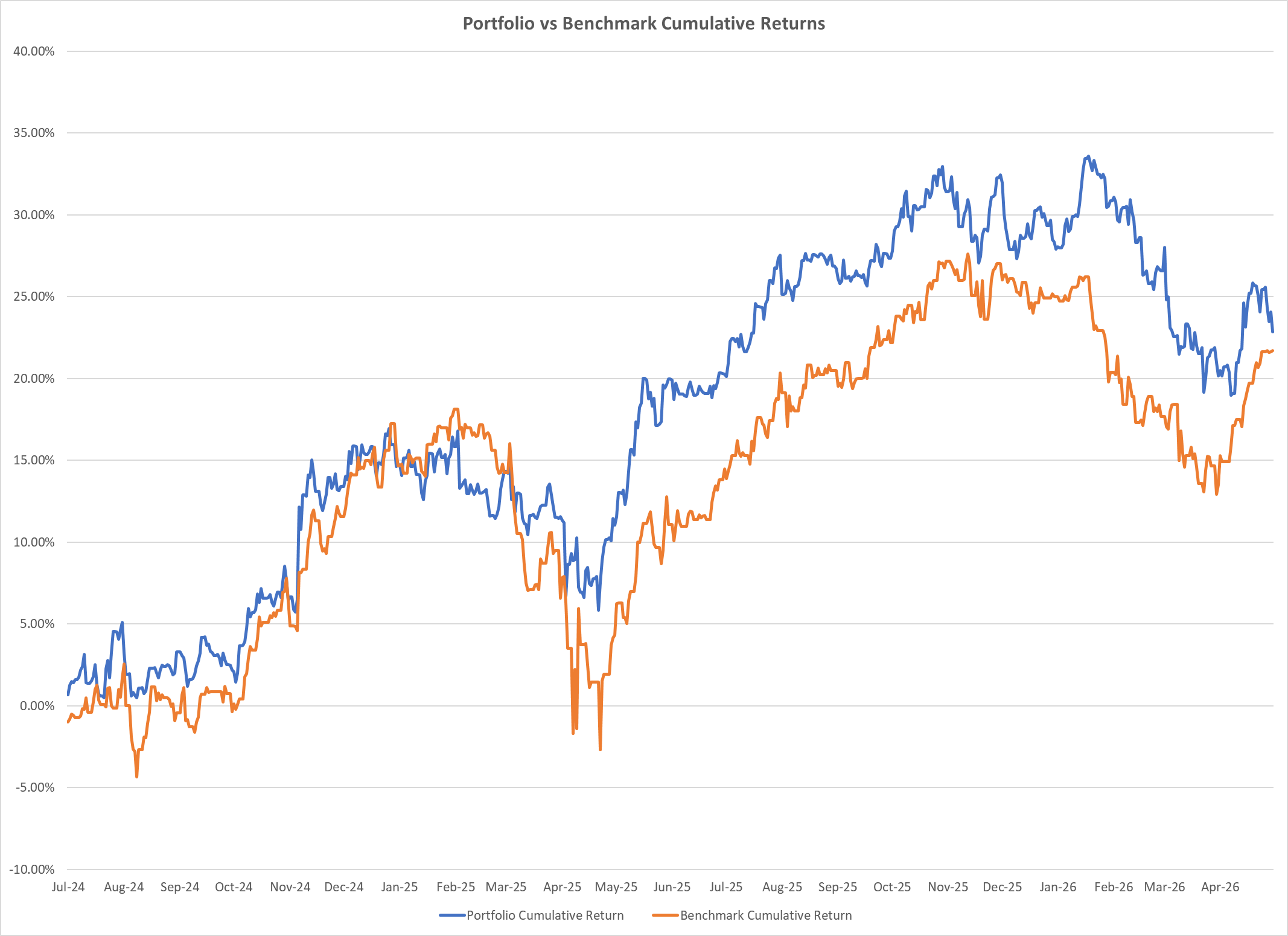

- Sustained outperformance

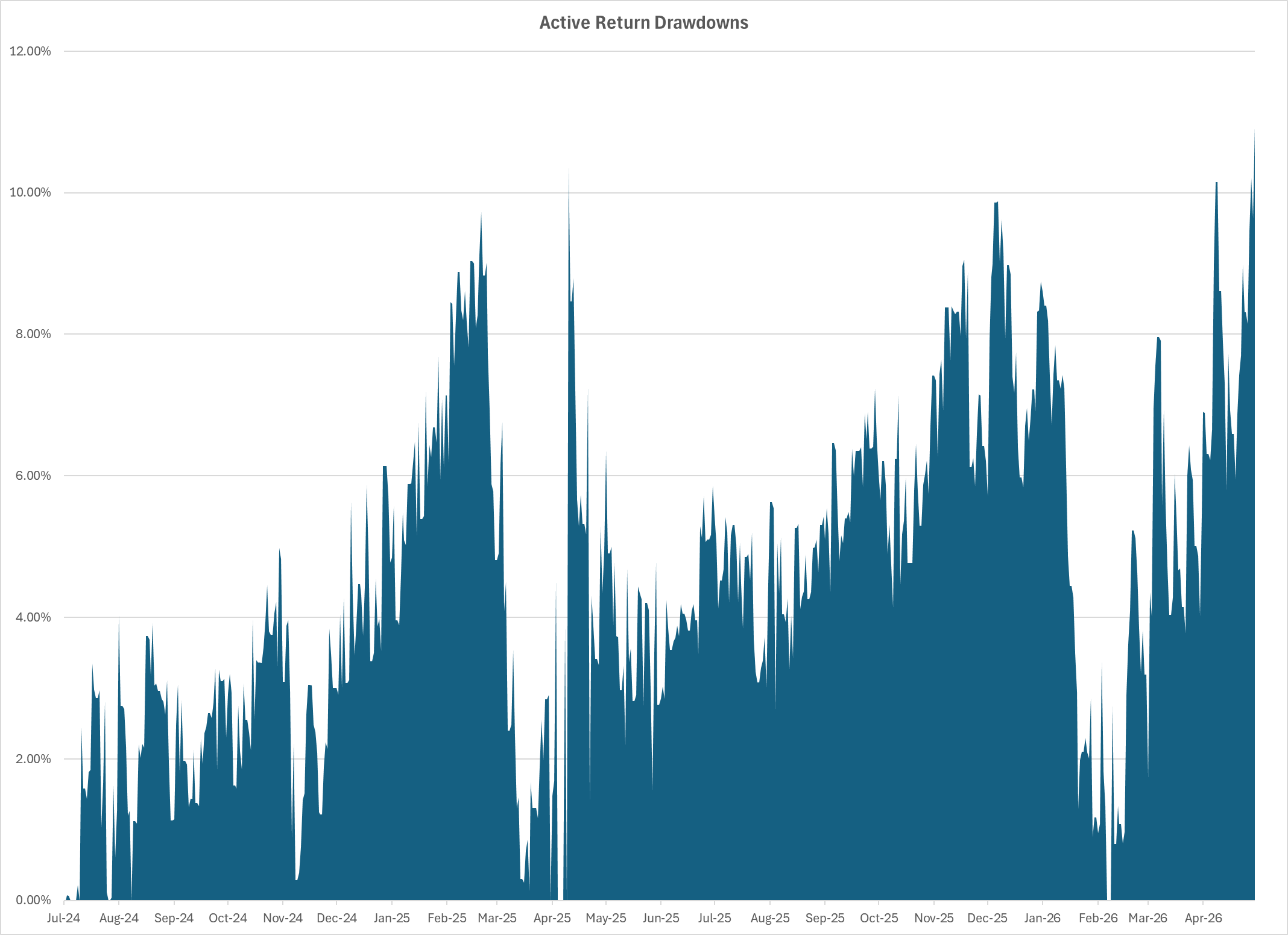

- Positive active return accumulation vs SPY AUD

- High-single digit annualized alpha

- Much lower max drawdown profile vs benchmark

- Lag vs SPY AUD benchmark has been contained to <1000bps usually

Takeaway

These are strong performance metrics by any institutional standard.

Disclosures and Disclaimers

Past performance ≠ future results. Not investment advice. See full Disclaimer.

Comments ()