SpaceX: Is The Starlink TAM Overstated? A Critical Valuation Review (Archive)

SpaceX faces significant valuation risks despite its growth potential and Starlink market share.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. I also publish full 5-Minute Pitches on this site. This will be behind a paywall, accessible to Hunter Tier members.

Elevator Pitch

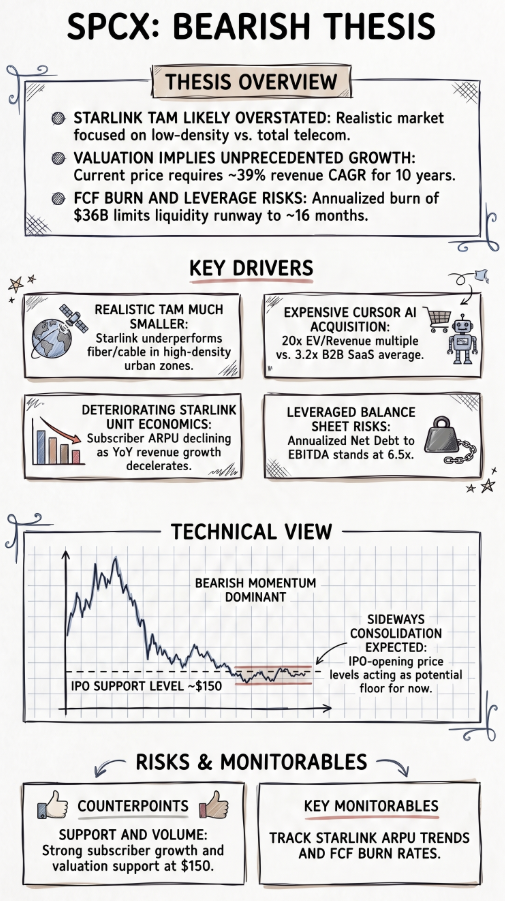

- SpaceX claims a massive total addressable market for Starlink, but this figure likely overstates potential revenue by ignoring competitive disadvantages in high-density urban areas.

- The company's decision to fund the expensive acquisition of Cursor with stock suggests management may believe shares are fully valued.

- High cash burn rates and a significant debt load create financial pressure, leaving the company with a limited runway until further financing is required.

- To justify its valuation, SPCX requires an unprecedented revenue growth rate of 39% CAGR over the next decade.

Read the full article here.