Marvell: Set To Win From Hyperscalers' Custom Chip Programs (Archive)

Marvell is primed for explosive custom AI chip growth, despite premium valuation risks.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. I also publish full 5-Minute Pitches on this site. This will be behind a paywall, accessible to Hunter Tier members.

Elevator Pitch

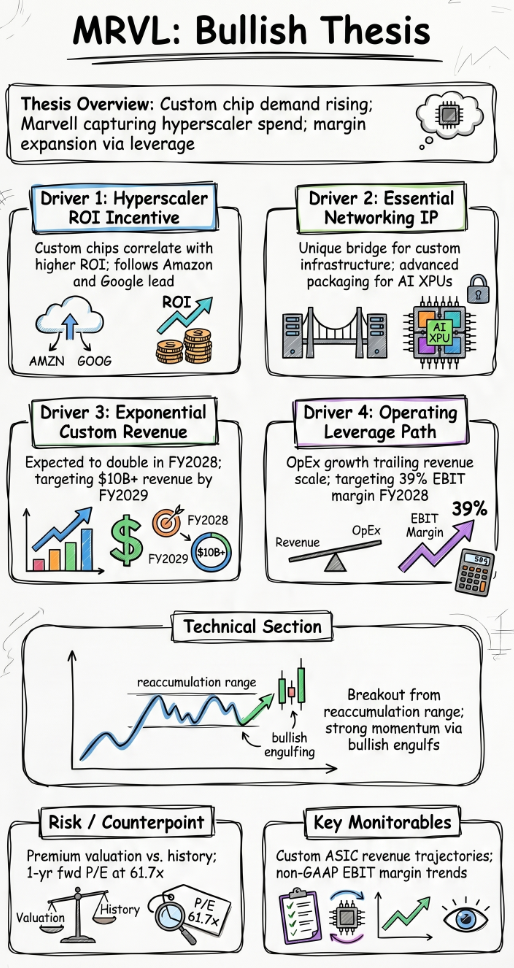

- Marvell is positioned for multi-year high revenue growth as hyperscalers expand custom chip programs and rely on MRVL's networking and advanced packaging IP.

- Custom chip revenue already contributes about $1.6B in TTM revenues. This is expected to grow to over $10B over the next 3 years.

- With ~45% YoY revenue growth and operating expenses growing in the mid-teens YoY range, there is a case for margin expansion. I expect almost 400bps over the next 2 years.

- MRVL trades at a premium to semiconductor peers, but consensus estimates imply a ~39% 6-yr fwd earnings CAGR that can support the high valuation, albeit with a low margin of safety.

- Technicals show a strong multi-year uptrend with a recent breakout from a re-accumulation base, suggesting the stock’s positive momentum is likely to persist.

Read the full article here.