Microsoft Is Paying Too Much In Capex To Drive Revenue Growth (Archive, Full Access)

Microsoft faces impending stock downside as aggressive AI infrastructure expenditures yield negative returns.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. I also publish full 5-Minute Pitches on this site. This will be behind a paywall, accessible to Hunter Tier members.

Elevator Pitch

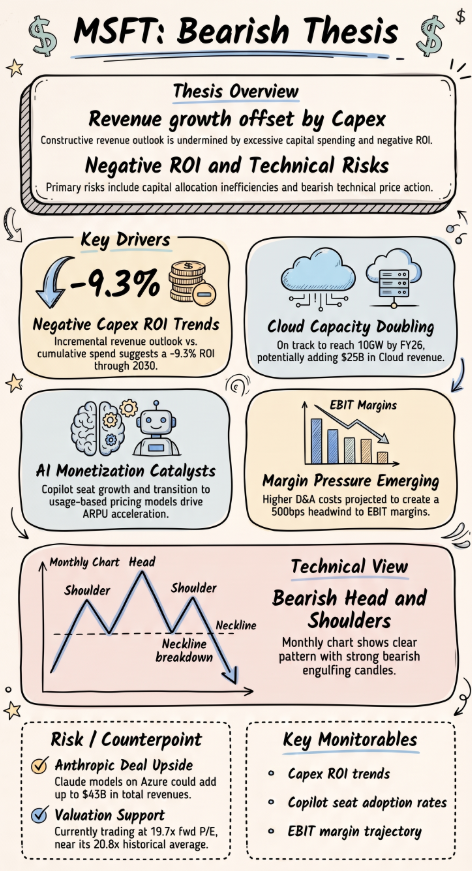

- Microsoft Corporation's data center capacity expansion to 10GW by FY26 is projected to accelerate Cloud revenue growth by 12.4% to 21.3%, aided by the Anthropic Azure AI Foundry deal.

- Average revenue per user for Office 365 can surprise to the upside, as Copilot adoption drives a transition toward consumption-based and usage-based compute pricing models.

- Aggressive capital expenditure projected to reach $190B by the end of CY26 carries an estimated negative ROI of -9.3%, signaling that Microsoft is overpaying for revenue growth.

- Accelerated depreciation and amortization costs from massive AI infrastructure outlays threaten to create a 500bps headwind to EBIT margins over the next couple of years.

- Despite trading at a slight 1-year forward P/E discount to peers and historical averages, a classic head-and-shoulders technical pattern on the monthly chart points to impending stock downside.

Read the full article here.