ServiceNow Q1 Preview: The Earnings Growth It Needs Is Too High To Justify A Buy (Archive)

AI disruption, healthy growth, and a demanding valuation hurdle shape my cautious ServiceNow view.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. 5-Minute Pitches published only this site will not be disseminated anywhere else and will remain behind a paywall, accessible only to Hunter Tier members.

Elevator Pitch

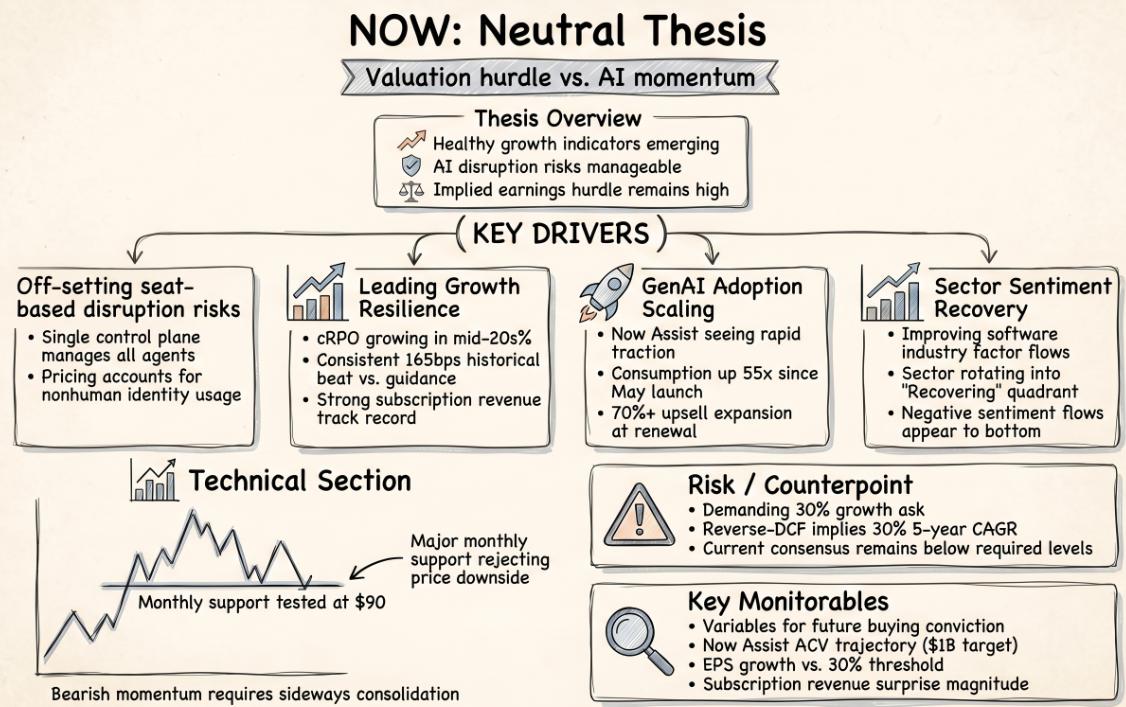

- ServiceNow faces AI-driven disruption risks but is adapting with hybrid pricing and strong AI product adoption.

- Key indicators such as remaining performance obligations indicate a healthy mid-20s% growth outlook, supported by the rapid uptake of Now Assist packs.

- Despite trading at a historical discount, a reverse-DCF-style analysis reveals a challenging implied 30% 5-year earnings CAGR needed to justify its current market price.

- Technicals show NOW stock at a major long-term support after a sharp selloff, suggesting downside may be limited but bearish momentum may cap near-term upside potential.

Read the full article here.