Oracle: Risks To Watch For In Q4 And Beyond (Archive)

Oracle’s OpenAI‑heavy backlog and aggressive AI capex create long‑dated, uncertain returns.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. I also publish full 5-Minute Pitches on this site. This will be behind a paywall, accessible to Hunter Tier members.

Elevator Pitch

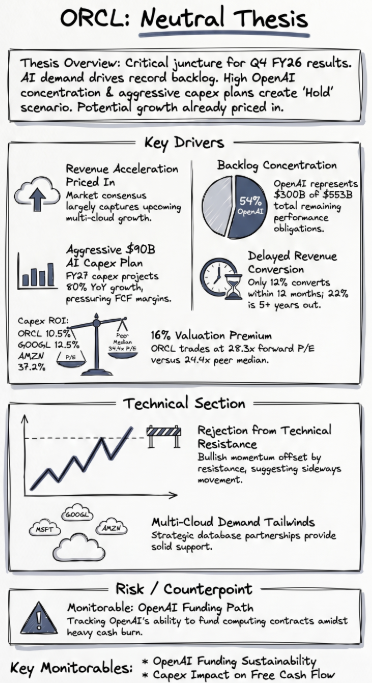

- Oracle Corporation’s record $553B RPOs (backlog) are heavily concentrated in OpenAI, with a large portion scheduled to convert into revenue only after several years.

- OpenAI’s funding needs, projected heavy cash burn, and missed internal targets create uncertainty for Oracle’s backlog-to-revenue conversion.

- ORCL’s aggressive AI capex plan boosts growth but pressures free cash flow and may generate returns below long‑run equity market expectations after inclusion of costs.

- Revenue should accelerate in the next two quarters on AI and multicloud demand, but Oracle’s history of minimal guidance and results surprise suggests this is mostly priced in.

- ORCL stock trades at a sizable 1-yr FWD P/E premium to AI infrastructure and software peers. The common shares seem to have better prospects than the 6.5% yielding preferred share class.

Read the full article here.