Nvidia Looks Undervalued, But That Doesn't Make Me More Bullish (Archive)

Undervalued juggernaut facing emerging margin and custom-chip headwinds despite explosive growth.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. I also publish full 5-Minute Pitches on this site. This will be behind a paywall, accessible to Hunter Tier members.

Elevator Pitch

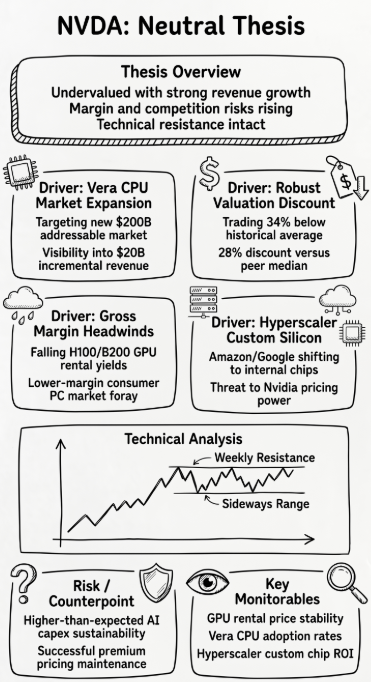

- Nvidia Corporation trades at a 1-yr fwd P/E below its history and peers. Its implied growth ask rate is also undemanding.

- Revenue growth near 85% could persist as Nvidia expands into CPUs. And Foxconn supplier data indicates strong AI demand ahead.

- Falling GPU rental prices and entry into low-margin consumer PCs could pressure Nvidia’s currently high gross margins.

- Growing adoption of custom AI chips by hyperscalers like Amazon and Google can threaten Nvidia’s long-term pricing power and data center share.

- NVDA's chart shows a failed breakout and a return to a wide trading range, suggesting choppy, sideways price action despite strong fundamentals.

Read the full article here.