Nvidia's Customers Are Quietly Building Alternatives (Archive, Full Access)

Nvidia’s trillion‑dollar AI pipeline offsets rising customer insourcing and near‑term technical downside.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. 5-Minute Pitches published only this site will not be disseminated anywhere else and will remain behind a paywall, accessible only to Hunter Tier members.

Elevator Pitch

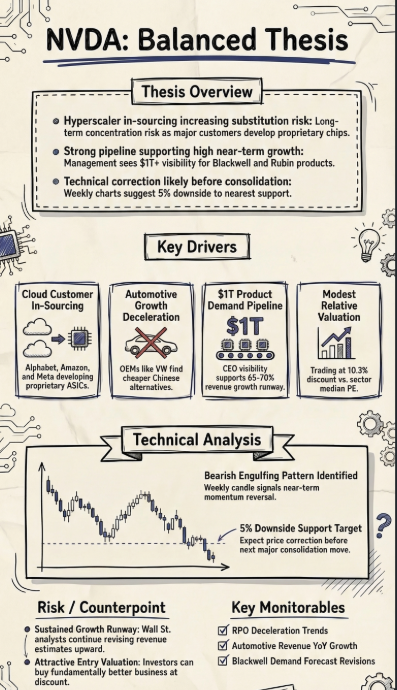

- Nvidia’s largest cloud customers are accelerating in-house chip efforts, increasing long-term substitution risk despite today’s exceptional AI demand visibility.

- Automotive revenue growth is already slowing as OEMs explore cheaper Chinese alternatives, hinting at how pricing pressure could eventually migrate to Nvidia’s core segments.

- Management now sees a one trillion dollar Blackwell and Rubin demand pipeline, reinforcing expectations for unusually strong revenue growth over the next several years.

- Street estimates for Nvidia’s revenue and earnings have been revised sharply higher, yet the stock trades at a modest valuation discount versus its historical premium to peers.

- Technicals show a bearish engulfing pattern on the weekly chart, implying roughly 5 percent near-term downside before the next potential consolidation zone.

Read the full article here. (This link is not behind Seeking Alpha's paywall).