Micron Says Go Big Or Go Home As It Ramps Up Capex Far More Than Peers (Archive, Full Access)

Micron’s AI memory bonanza is compelling, but aggressive capex keeps the rating at Hold.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. 5-Minute Pitches published only this site will not be disseminated anywhere else and will remain behind a paywall, accessible only to Hunter Tier members.

Elevator Pitch

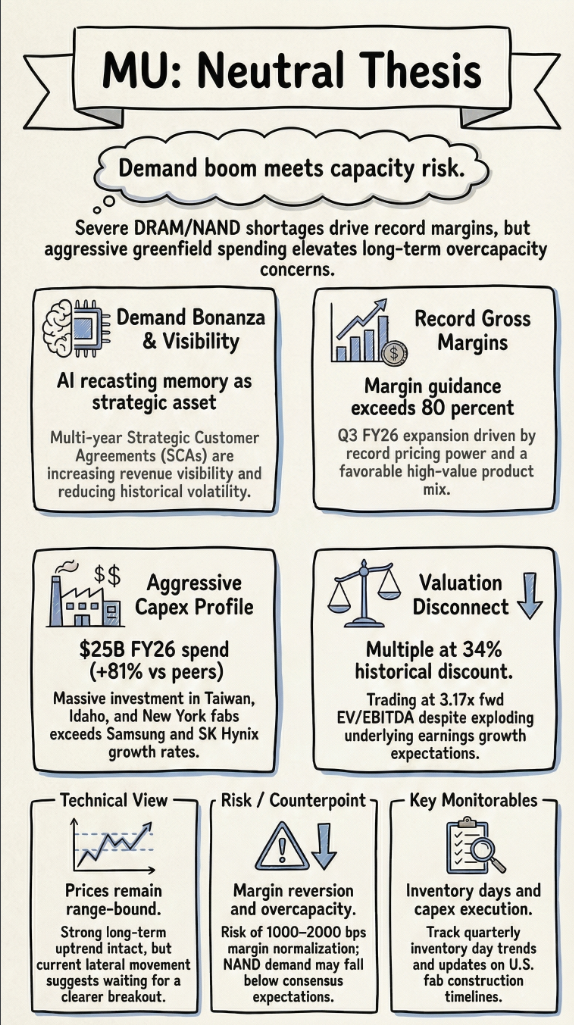

- Micron is benefiting from acute DRAM and NAND shortages, driving a demand and pricing bonanza supported by multi-year Strategic Customer Agreements that enhance revenue visibility and reduce volatility.

- Record gross margins guided above 80 percent reflect higher prices, a favorable mix, and lower costs, but may normalize as we may be near peak margins.

- Micron’s FY26 and FY27 capex plans, including Tongluo and new U.S. fabs, imply an unusually aggressive greenfield expansion that raises long-term overcapacity risk versus memory peers.

- Despite strong earnings growth expectations, Micron trades at a discounted forward EV/EBITDA multiple versus its historical median, creating a compelling but cycle-sensitive valuation setup.

- Technicals show Micron in a strong uptrend but currently range-bound, suggesting investors may hold existing positions while waiting for a clearer breakout before adding exposure.

Read the full article here. (This link is not behind Seeking Alpha's paywall).