Dell: Why It's Not A Buy Despite A $43 Billion AI Backlog (Archive, Full Access)

Explosive AI demand meets fair valuation and looming PC and margin headwinds.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. 5-Minute Pitches published only this site will not be disseminated anywhere else and will remain behind a paywall, accessible only to Hunter Tier members.

Elevator Pitch

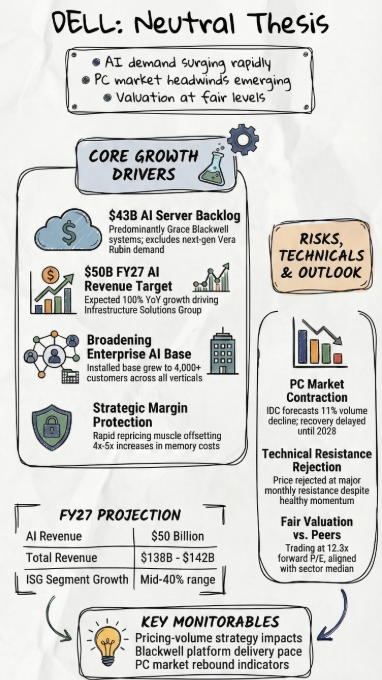

- Dell’s AI server business is seeing explosive demand, with a $43 billion backlog and rapidly growing remaining performance obligations.

- AI revenue could reach $50 billion in FY27, driving strong Infrastructure Solutions Group growth, while Client Solutions faces muted growth from a shrinking PC market.

- Dell is offsetting surging memory costs through rapid repricing, protecting gross margins so far with limited demand destruction.

- Dell maintains roughly 16% global PC shipment share, balancing AI growth with cyclical pressure in its traditional PC segment.

- Dell’s valuation near a 12.3x forward PE and rising earnings expectations suggest a fundamentally stronger business at a fair multiple.

Read the full article here. (This link is not behind Seeking Alpha's paywall).