Credo: The Market Hasn't Fully Priced In The DustPhotonics Deal's Implications (Archive, Full Access)

DustPhotonics deal supercharges Credo’s optics growth, margins, and still-undervalued stock.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. 5-Minute Pitches published only this site will not be disseminated anywhere else and will remain behind a paywall, accessible only to Hunter Tier members.

Elevator Pitch

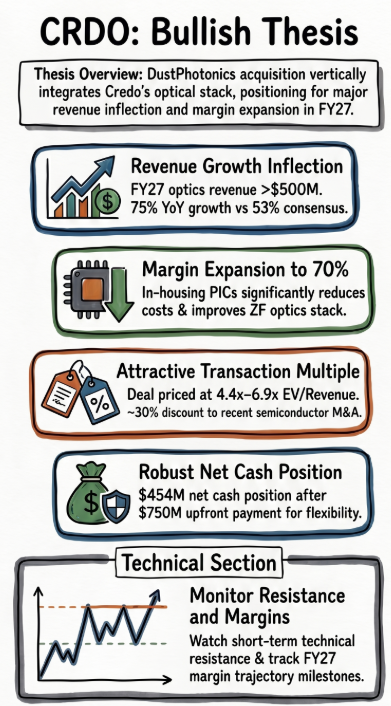

- Credo’s DustPhotonics acquisition should lift optics revenue to over $500M in FY27 and support revenue growth above 75% year-over-year.

- Bringing silicon photonics PICs in-house enables a more integrated ZF optics stack and can improve long-term gross margins toward 70%.

- The implied 4.4x–6.9x EV/revenue transaction multiple for the deal is attractive, given the comps of recent semiconductor and optics M&A transactions and valuation benchmarks.

- Credo’s balance sheet remains strong after the $750M upfront cash payment, with an estimated $454M net cash position supporting future strategic flexibility.

- Despite a sharp recent rally, CRDO still trades below the peer median 1-year forward P/E, although the stock’s approach to resistance may cause a short-term pause.

Read the full article here.