Credo: Optics Ramp, Margin Upside And Bullish Charts Point To More Upside (Archive)

Credo’s optics ramp, margin expansion, and technicals still justify a bullish buy rating.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. I also publish full 5-Minute Pitches on this site. This will be behind a paywall, accessible to Hunter Tier members.

Elevator Pitch

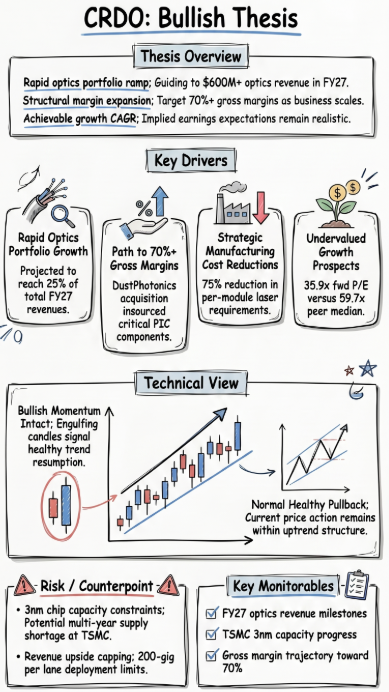

- Credo is rapidly ramping its optics portfolio, with management guiding to more than $600M of optics revenue in FY27.

- Next generation 1.6T data center networks depend on 3nm chips, and 3nm capacity constraints could cap Credo’s longer term revenue upside.

- The DustPhotonics acquisition brings photonic integrated circuits in-house and reduces per module laser count by 75 percent, supporting structurally higher gross margins.

- Credo’s gross margin outlook remains strong, with management guiding to around 68 percent near term. I expect further improvement to 70%+ as the optics business scales up.

- Even after its run, CRDO's implied multi-year earnings growth expectations still look achievable relative to its margin expansion and revenue growth potential.

Read the full article here.