Broadcom Q2: Undervalued After The Post-Earnings Selloff (Archive)

There's AI capex scrutiny and margin pressure, but valuation discount supports patient holders.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. I also publish full 5-Minute Pitches on this site. This will be behind a paywall, accessible to Hunter Tier members.

Elevator Pitch

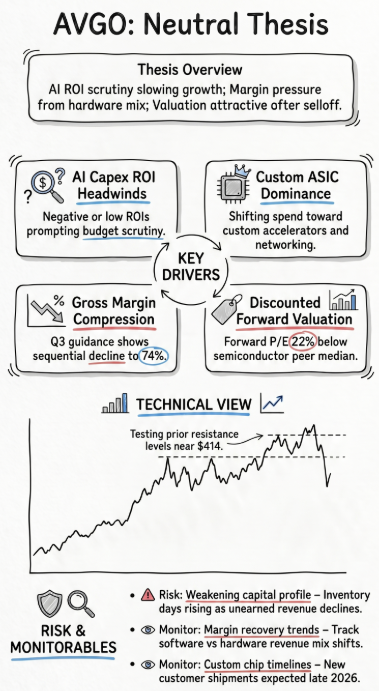

- Hyperscalers' AI capex ROI looks only roughly in line with equity market return expectations. This may prompt greater scrutiny of AI spend from here on.

- Tighter scrutiny of AI budgets may pressure Broadcom's pace of growth, but rising demand for custom AI accelerators and networking should partially offset slower generic accelerator spending.

- A mix shift toward lower-margin AI hardware is pressuring Broadcom's gross margins and weakening its working capital profile.

- Broadcom trades at a notable discount to semiconductor peers on forward P/E despite historically commanding a premium multiple.

- AVGO's long-term uptrend remains intact, but the recent post-earnings selloff has paused bullish momentum near a key resistance level.

Read the full article here.