Blue Owl Capital: The Math On What's A Fair Downside

Math suggests OWL’s >40% selloff overshoots realistic AUM and fee headwinds.

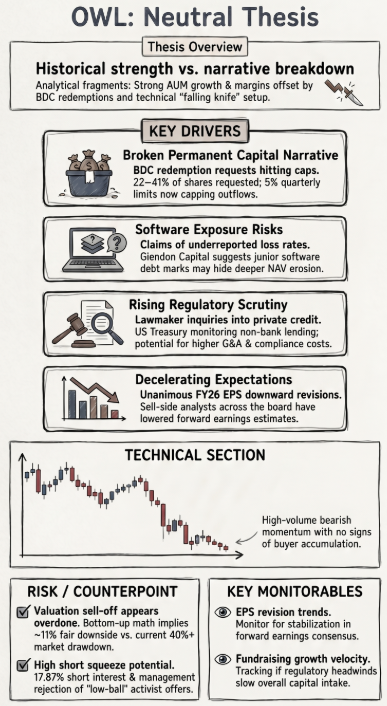

Elevator Pitch

Blue Owl Capital (OWL) is a very interesting situation because from a historical financials print perspective, nothing seems wrong. But the market has been strongly reacting to expectations of future weakness. Here's how I'm making sense of it:

- Blue Owl shows strong historical AUM, fee revenue, and margin growth, but the stock is selling off on concerns about future portfolio losses and private credit valuations.

- Large redemption requests at OCIC and OTIC have cracked confidence in Blue Owl’s “permanent capital” narrative, even though quarterly redemption caps limit near-term AUM and NAV erosion.

- Activist low-ball tenders and elevated short interest highlight a very bearish sentiment, yet management's suggestion to reject the offer and the risk of a short squeeze increase chances of upside.

- Regulatory scrutiny and Treasury attention on private credit risks may raise costs and slow growth, adding another overhang for Blue Owl and its peers in the near term.

- Blue Owl now trades at a much steeper discount to alternative-asset peers, and bottom-up math suggests the recent selloff is larger than implied by realistic fee and AUM hits.