Barrick Mining: IPO Spinoff Dream Hits Royalty Shocker And Margin Squeeze (Archive)

IPO upside dulled by disputes, hidden royalties, rising costs, and richer valuation.

This 5-Minute Pitch was originally published on Seeking Alpha. It is shared here to showcase my work and track record. 5-Minute Pitches published only this site will not be disseminated anywhere else and will remain behind a paywall, accessible only to Hunter Tier members.

Elevator Pitch

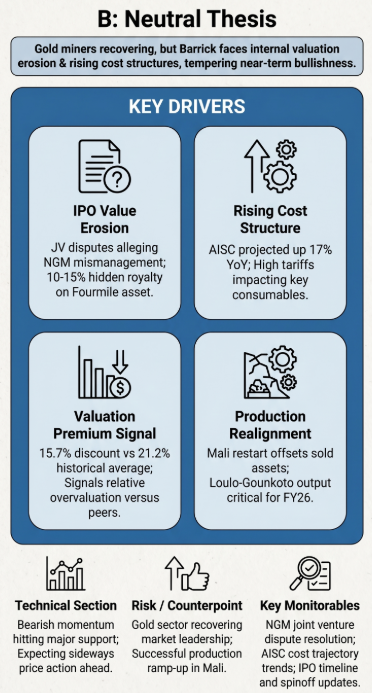

- Partner disputes with Newmont over Nevada Gold Mines and a Fourmile royalty to Teck threaten Barrick’s planned IPO timing and value realization.

- Loulo-Gounkoto’s restart in Mali is expected to roughly offset production lost from Hemlo and Tongon asset sales by FY26.

- Rising all-in sustaining costs, driven by higher Mali taxes, royalties, and tariffs, are likely to pressure Barrick’s free cash flow margins.

- Barrick now trades at a smaller discount to peers than its historical norm, making the relative valuation perspective less attractive.

- Technical and sentiment indicators show balanced bull and bear forces, pointing to a higher probability of sideways trading around current support.

Read the full article here.