AMD: Why I'm Slapping A Strong Sell On This Market Darling (Archive, Full Access)

AMD’s overhyped AI story masks decelerating growth, margin risk, and rich valuation.

This 5-Minute Pitch was originally published on Seeking Alpha before the launch of the Hunting Alphas website. It is shared here to showcase my previous work and track record. New 5-Minute Pitches published on this site will not be disseminated anywhere else.

Elevator Pitch

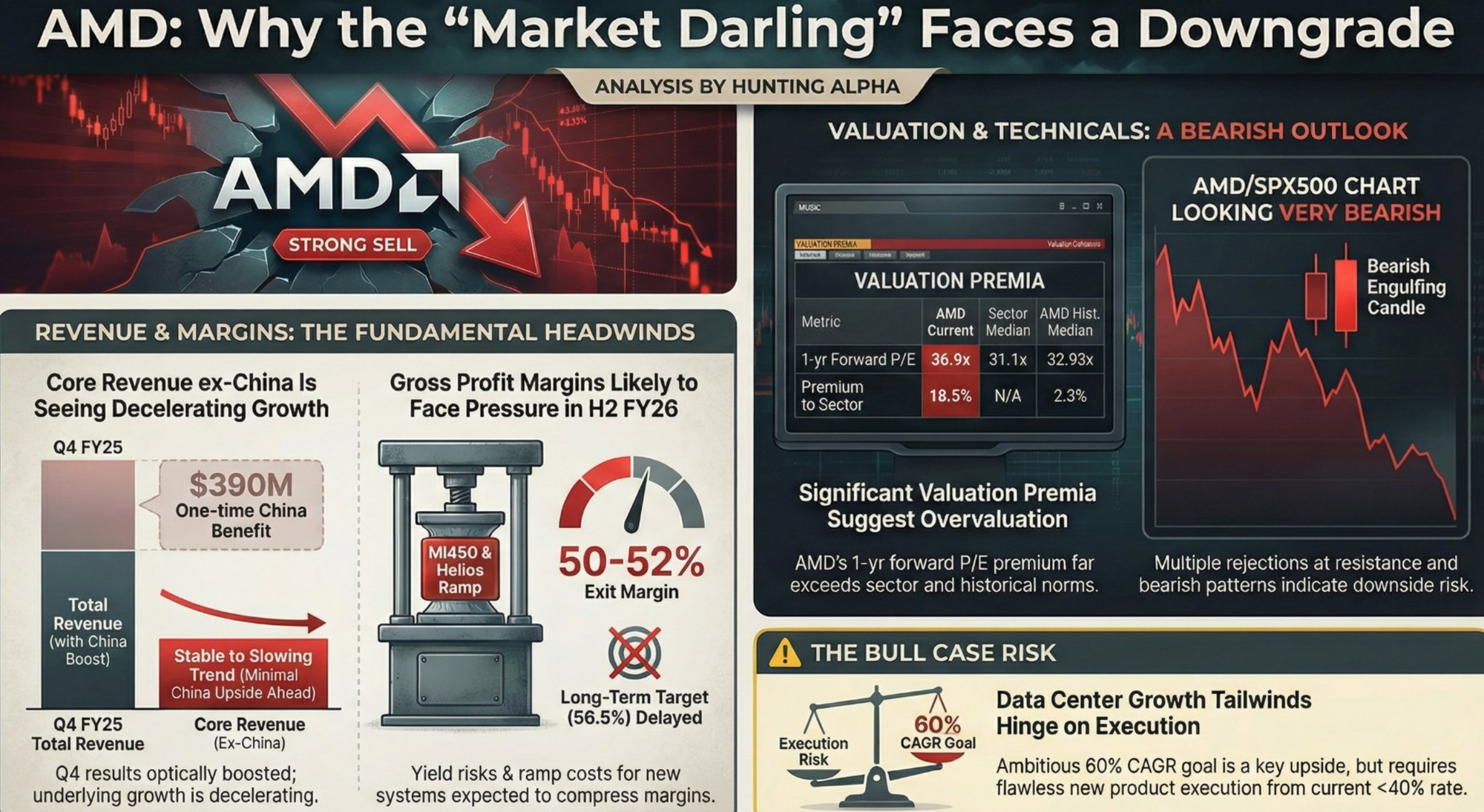

- Advanced Micro Devices, Inc.’s core revenue growth excluding a one-time China boost is stable to decelerating, despite headline results suggesting a stronger acceleration.

- AMD management guides for minimal China contribution ahead, warning investors not to assume further upside from this highly uncertain market.

- Gross margins face pressure in H2 FY26 as AMD ramps MI450 and Helios, with yields and ramp costs likely delaying long-term margin targets.

- AMD’s valuation screens rich versus peers and its own history, with the stock trading at a higher-than-usual forward P/E premium.

- Data center growth could surprise positively, but AMD’s ambitious 60% CAGR goal hinges on successful execution and broader adoption of new product launches.

Read the full article here. (This link is not behind Seeking Alpha's paywall).

Disclosures and Disclaimers

Past performance ≠ future results. Not investment advice. See full Disclaimer.

Comments ()